Roth Madness 2026: The Ultimate Roth Conversion Showdown

Every March, brackets take over the world — so we built one for Roth conversions.

Roth Madness is a head‑to‑head tournament of Roth conversion strategies, modeled using current tax law, Income-Related Monthly Adjustment Amount (IRMAA) impacts, Social Security tax interactions, and long‑term net present value (NPV) outcomes. Advisors get a front‑row seat to see how different conversion paths perform over a lifetime.

Rules of Roth Madness

Click here to view the rules of Roth Madness

One Client Profile, Three Scenarios

All strategies use the same household fact pattern to ensure apples‑to‑apples comparisons. Each round will have a different planning wrinkle.

Four Competing Strategies

- 1‑Year Conversion

- 5‑Year Conversion

- 10‑Year Conversion

- Bracket Ride (convert up to 24% annually until fully converted)

Four Scoring Categories

- Roth IRA Value at Death

- Lifetime Taxes Paid

- IRMAA and Social Security Tax Impact

- Total NPV

Final Champion

The strategy with the highest overall NPV becomes the Roth Madness Champion.

Client Profile

- IRA Owner Age: 55

- Spouse Age: 53

- Filing Status: Married Filing Jointly

- Annual Income: $325,000

- 2026 IRA Balance: $1,200,000 (7% ROI)

- Savings Balance: $500,000

- Retirement Age: 65

- Retirement Annual Income: $125,000

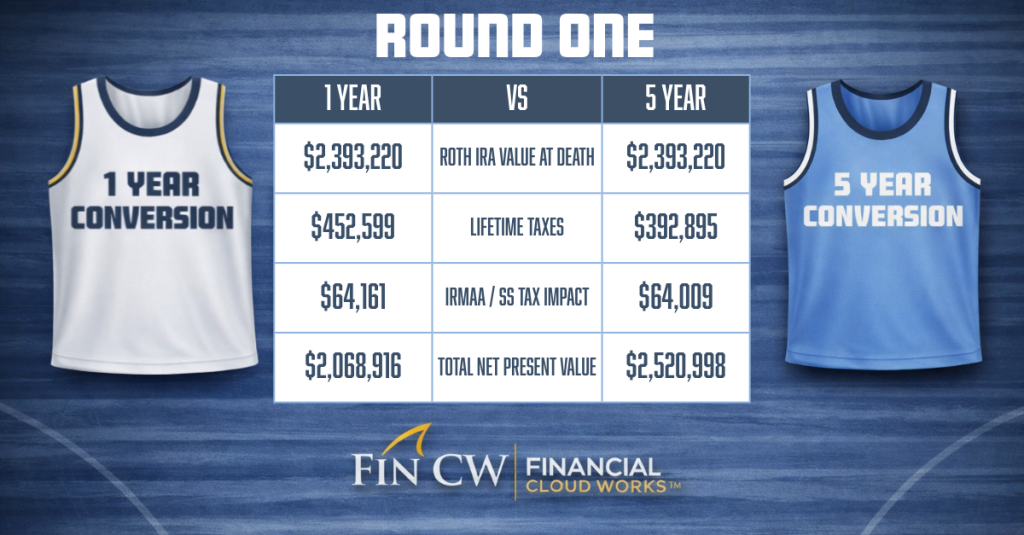

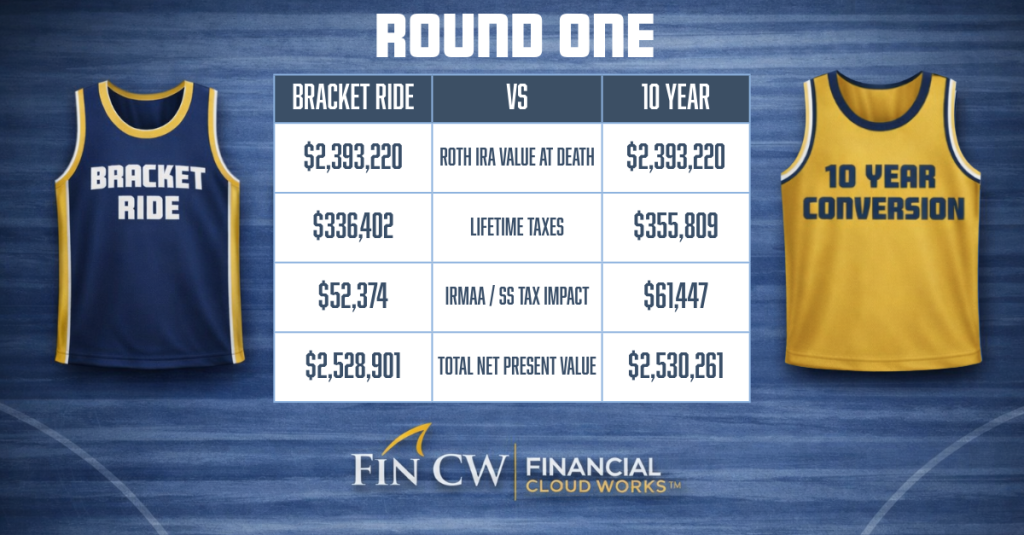

Round One: Clients Live to Age 86

Watch the Round One Recap below.

View Round One Breakdown

In Round One, our baseline assumption is that the clients will live to age 86. There are no additional spending needs beyond their annual income.

1 Year vs 5 Year Conversion Findings: Almost $60K less taxes are paid by spreading the conversion out over 5 years. It is slightly better from an IRMAA and Social Security Tax impact standpoint but not by much. The Total NPV of the 5 Year conversion model is $452K better than the 1 Year model.

Bracket Ride vs 10 Year Conversion Findings: Bracket Ride yields almost $20K less in taxes paid than the 10 Year Conversion Model but loses the IRMAA / Social Security Tax Impact battle by $9K. This ultimately leads to the 10 Year Conversion’s small victory of $1,360 better total NPV.

Round One Overall Winner: It was neck and neck, but 10 Year Conversion takes the crown for the first round, showcasing the largest NPV of all models.

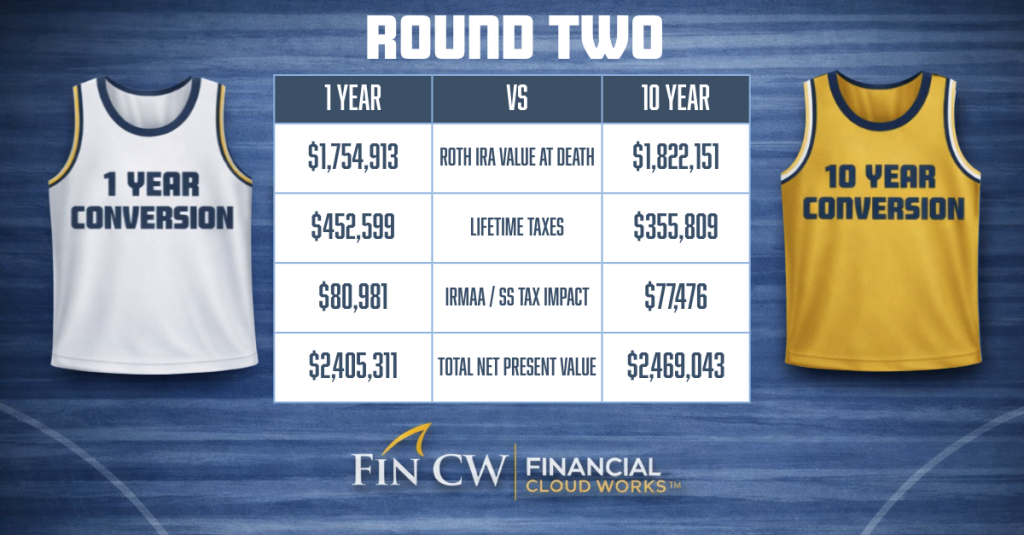

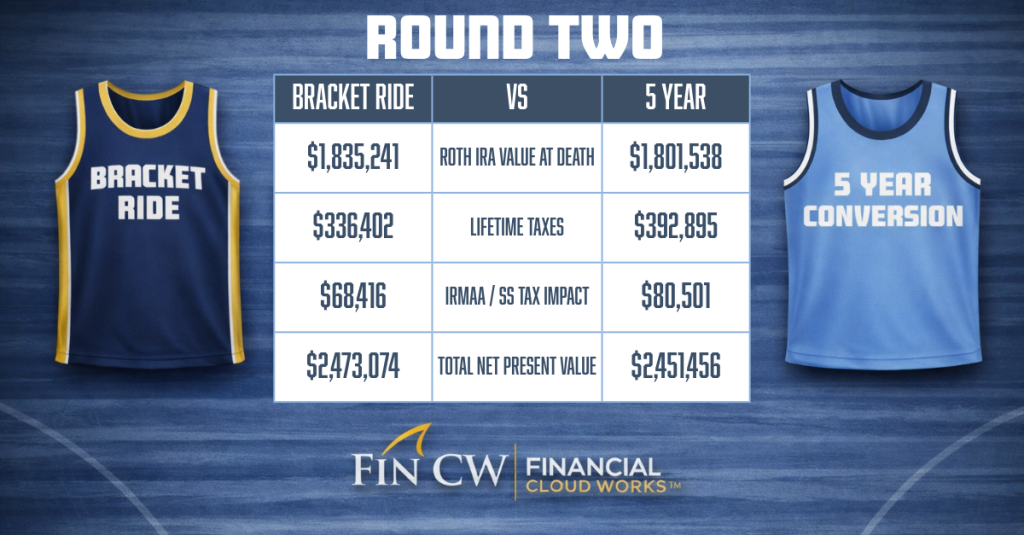

Round Two: Annual Spending Needs Rise to $100K at Age 70

View Round Two Breakdown

In Round Two, we assume the clients live to age 86 and require an additional $100K per year beginning at age 70, on top of their base income.

1 Year vs 10 Year Conversion Findings: 10 Year Conversion takes the win in every category except IRMAA and Social Security impact in this matchup. By spreading conversions over a decade, the client reduces taxable spikes and saves nearly $100K in lifetime taxes. The strategy also delivers a stronger long‑term outcome, with Total NPV coming in $63K higher than the 1 Year Conversion.

Bracket Ride vs 5 Year Conversion Findings: Bracket Ride nearly swept every category, with the lone exception being IRMAA and Social Security impact. Because this strategy stretches conversions over 12 years, the larger conversion years fall within Medicare’s two‑year IRMAA look‑back window. Those elevated taxable‑income years trigger higher Medicare premiums, giving the 5 Year Conversion a $12K advantage in this single category. Even so, that IRMAA edge isn’t enough to overcome Bracket Ride’s stronger overall NPV performance.

Round Two Overall Winner: 10 Year Conversion and Bracket Ride were closely matched again in the Round Two comparison, but this time Bracket Ride takes the lead. It claims three out of four categories, with Roth Value at Death and Lifetime Taxes ultimately giving it the winning margin.

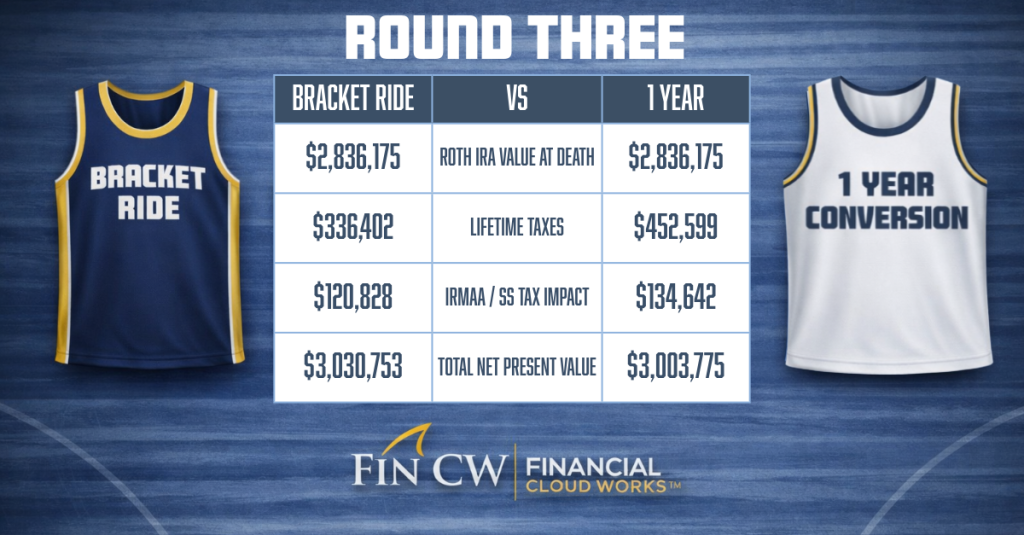

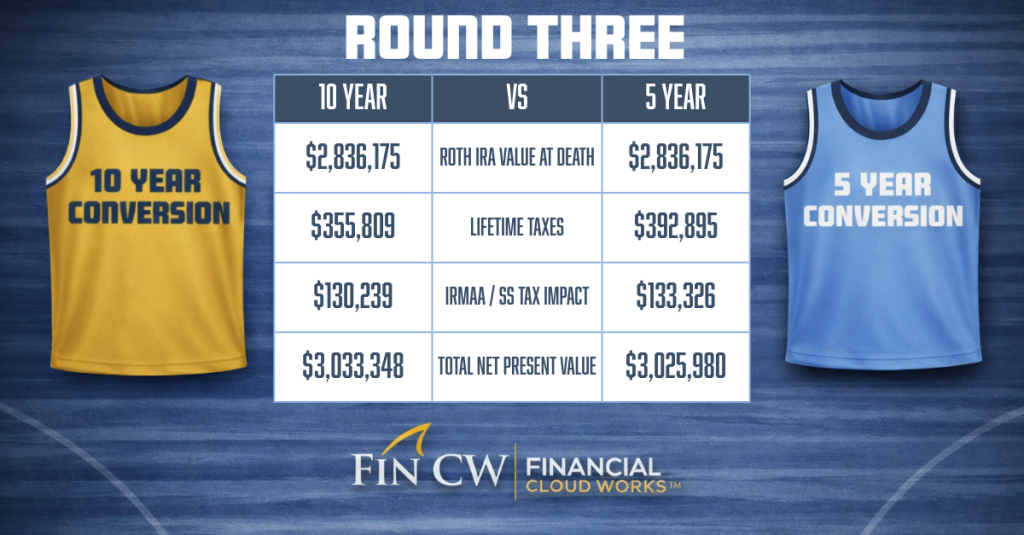

Round Three: Clients Live to Age 95

View Round Three Breakdown

In Round Three, our baseline assumption is that the clients will live to age 95. There are no additional spending needs beyond their annual income.

Bracket Ride vs 1 Year Conversion Findings: Like Round One, Roth IRA value at death ends in a draw. Bracket Ride wins Lifetime Taxes by $116K, while 1‑Year Conversion takes the IRMAA/SS category by $14K. The tiebreaker comes from overall efficiency: Bracket Ride wins Total NPV by $27K and advances.

10 Year Conversion vs 5 Year Conversion Findings: Roth IRA value at death is a draw. 10‑Year wins Lifetime Taxes by $37K, while 5‑Year edges out the IRMAA/SS category by $3K. The deciding metric is long‑term efficiency: 10‑Year wins Total NPV by $8K and advances.

Round Three Champion: With both earlier matchups coming down to Total NPV, the trend continues here: 10‑Year Conversion edges out the field on long‑term value, securing the win in Round Three and moving on.

Round Madness Champion

Watch the Round by Round Recap below.

View the Overall Champion Breakdown

10 Year Conversion: Ultimate Champion — Best Total NPV (2 of 3 Rounds)

- The 10‑Year Conversion required paying more taxes than Bracket Ride, but its full conversion was completed before Medicare’s two‑year IRMAA look‑back period began. That timing advantage gave it the ultimate edge, securing wins in two of three rounds.

Bracket Ride: Best Lifetime Tax Efficiency (3 of 3 Rounds)

- Bracket Ride stretched conversions over 12 years, which meant the 55‑year‑old client entered Medicare’s two‑year IRMAA look‑back window at ages 63 and 64. While spreading taxes over a longer timeline made Bracket Ride the most tax‑efficient strategy overall, those IRMAA events ultimately reduced its Total NPV, keeping it just behind the 10‑Year Conversion.

1 Year Conversion: Best IRMAA/SS Impact — Clean Sweep (3 of 3 Rounds)

- The 1‑Year Conversion swept the tournament in the IRMAA and Social Security tax‑impact category because the entire conversion was completed long before the client ever entered the IRMAA look‑back window. That early timing eliminated future Medicare surcharges — but it came at a cost. Compressing the entire conversion into a single year created the largest tax spike of any strategy, giving 1‑Year the highest total tax bill in all three rounds.

5 Year Conversion: Most Balanced — Middle‑Ground Performer

- The 5‑Year Conversion consistently ranked second in the IRMAA and Social Security tax‑impact category across all three rounds, finishing right behind the 1‑Year strategy. Converting over five years did cost the client $37K more in taxes compared to the 10‑Year approach, which is why it never secured a round win. Even so, it remained competitive — taking second place in Total NPV in Round Two and staying within striking distance of the 10‑Year strategy throughout the tournament. It didn’t dominate any single category, but it was never the weakest performer either.

So, what’s the “best” Roth conversion strategy? It depends.

Clients who want certainty — and don’t want to gamble on future tax hikes — may prefer converting sooner, even if it means a higher upfront tax bill. Others may be more comfortable spreading conversions out to avoid sticker shock while still moving toward their long‑term goals.

The good news is you don’t have to guess. You can model every scenario using your client’s actual numbers, compare the outcomes side‑by‑side, and let them choose the path that feels right for them.

Run a Roth Madness Scenario

Want to see how your client’s numbers stack up? We’ll run a custom Roth Madness bracket using your client’s real fact pattern and send you a report summary.

This is a powerful way to show clients the long‑term impact of different Roth strategies — and it’s completely free.

What’s Next

If you want to see how the modeling works behind the scenes. Schedule a demo to see how we can help you:

- Model multi‑year Roth strategies

- Compare bracket‑based conversions

- Forecast IRMAA and Social Security tax interactions

- Produce client‑ready reports in minutes

We’re offering a March Madness discount, schedule a demo to find out more!