Case 1 – Same Beneficiary, Owner Had Already Started RMDs

-

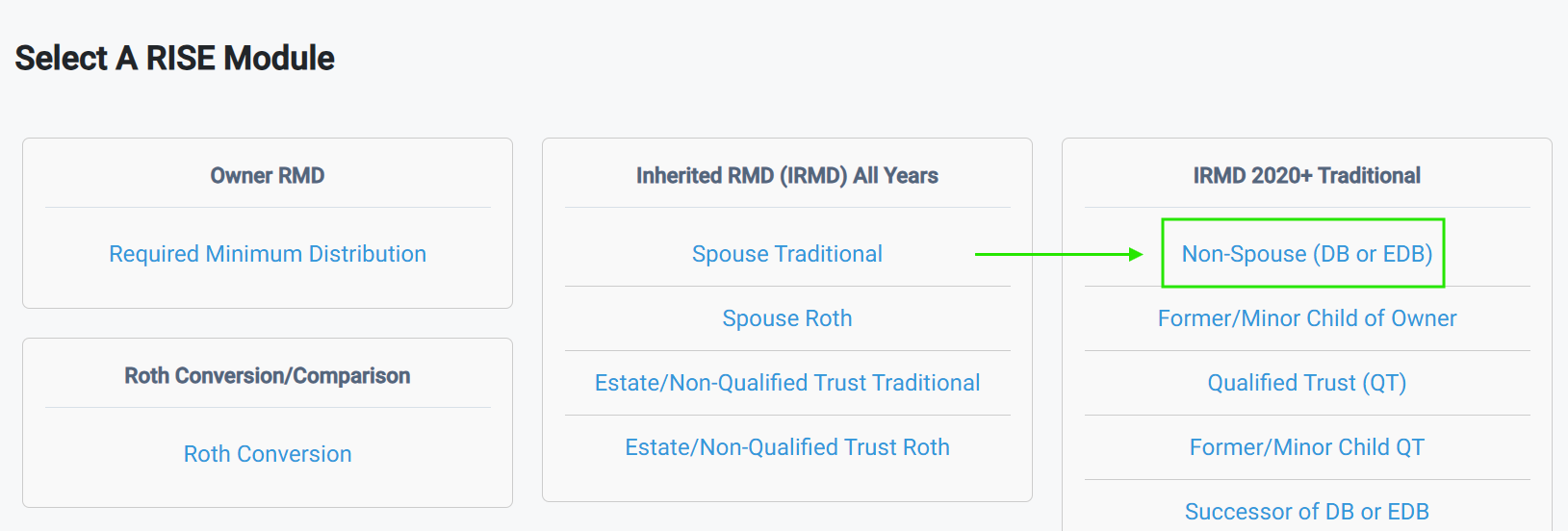

1Log in at fincw.com and access Break Analytics. Click the Non-Spouse (DB or EDB) module under IRMD 2020+ Traditional.

-

2Complete the General form. The Prepared For field should be the name of your client, the beneficiary.

-

3Complete the Deceased and Beneficiary form with these facts:

Deceased IRA Owner Birth Month and Year: 4/1945

Deceased IRA Owner Year of Death (2020-2025): 2025

Beneficiary Name: Jon Doe

Beneficiary Date of Birth: 1/1981

-

4Complete the Inherited IRA form. Use $500,000 for the Prior I-IRA Year End Value and keep 6% as the ROI. Skip Distribution Methods for now.

-

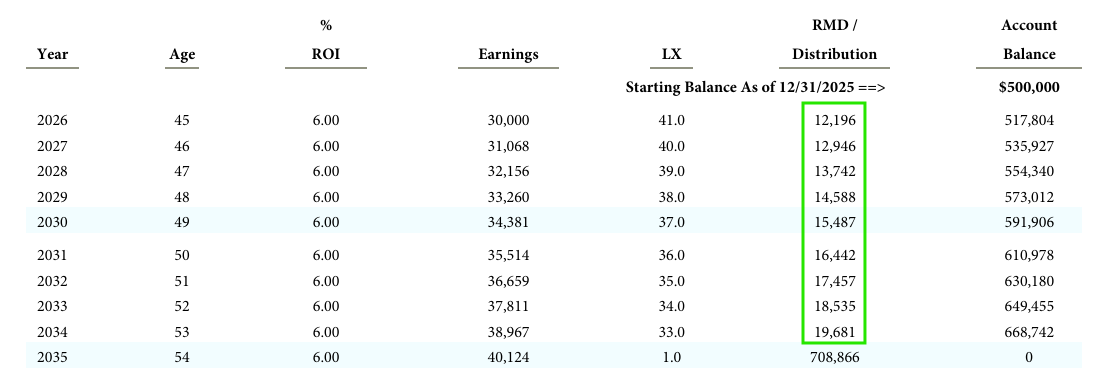

5Move to the Illustration/Analysis form and click Generate PDF. Go to page 3.

This client is still a Designated Beneficiary (DB) under the 10-year rule – but because the owner died on or after their RBD, annual RMDs are required in years 1-9 and the account is emptied by the end of year 10. The education on page 3 reflects this. This is the client who has an RMD due this year and may not know it.

One Last Change

Update the beneficiary date of birth

Keep everything the same. Update the Beneficiary Date of Birth to 4/1954 and generate the PDF.

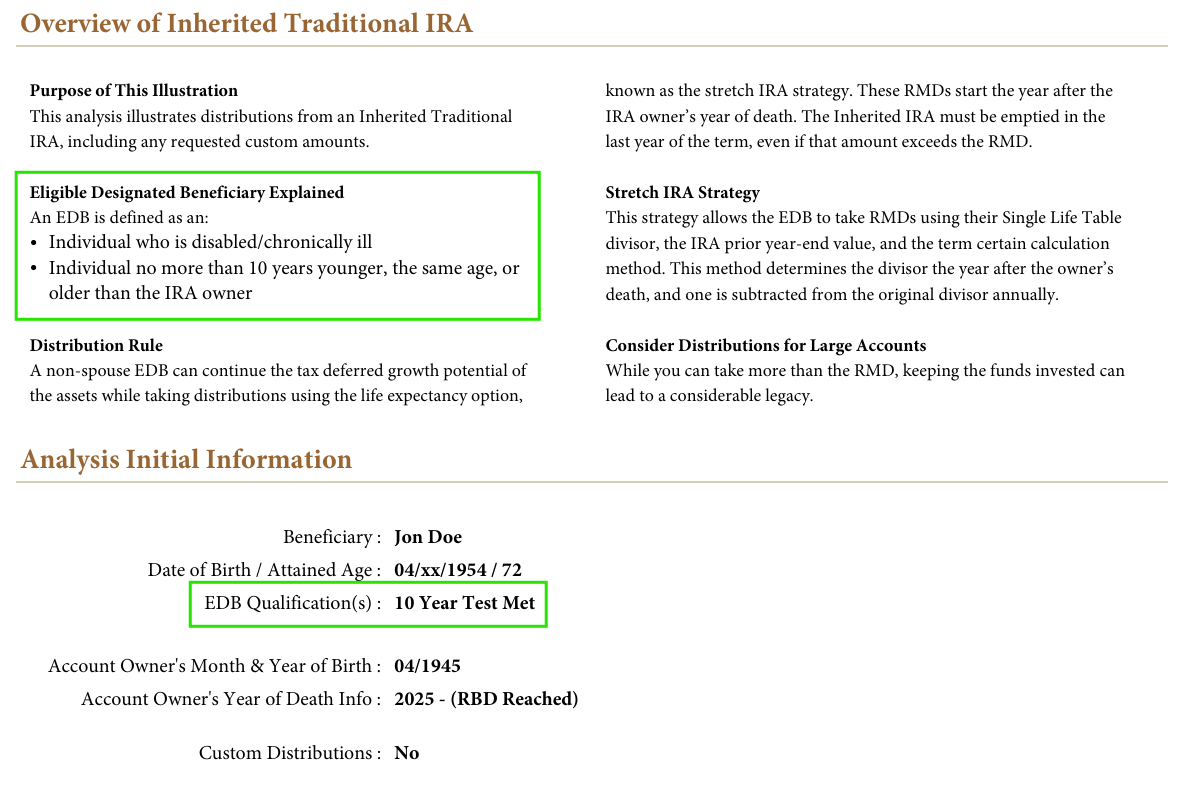

Page 3 changed entirely. This client is now a Non-spouse Eligible Designated Beneficiary (EDB) – they meet the 10 Year Test because they are not more than 10 years younger than the IRA owner. EDBs have the life expectancy option, which means distributions can extend over their life expectancy on a term-certain basis. The planning conversation for this client looks completely different from the first two.

A quick check of the beneficiary’s date of birth relative to the IRA owner’s date of birth can change the outcome entirely.

The IRS Plan

What you just ran is the IRS Plan – the distribution schedule the IRC requires if no strategy is selected. This is a useful starting point because it shows the minimum your client is required to do. From here you can help them build the Client Plan based on their specific situation and goals by selecting Custom Distributions or Distribution Smoothing (DBs only) in the Distribution Methods from Step 4.

Questions on navigating the software? Schedule with Thomas here

Want to walk through a client situation? Schedule with Patrick here